Introduction:

In the dynamic world of trading, the ability to adapt and comprehend market dynamics is foremost to staying ahead. In a recent dialogue with a seasoned trading strategist, we explored a fundamental question:

Do trading strategies become outdated or stop working?

Our conversation revolved around the complexities of strategy development (Curve Fitting), the impact of market cycles, and the resilience required to withstand the drawdowns.

The Pitfalls of Curve Fitting:

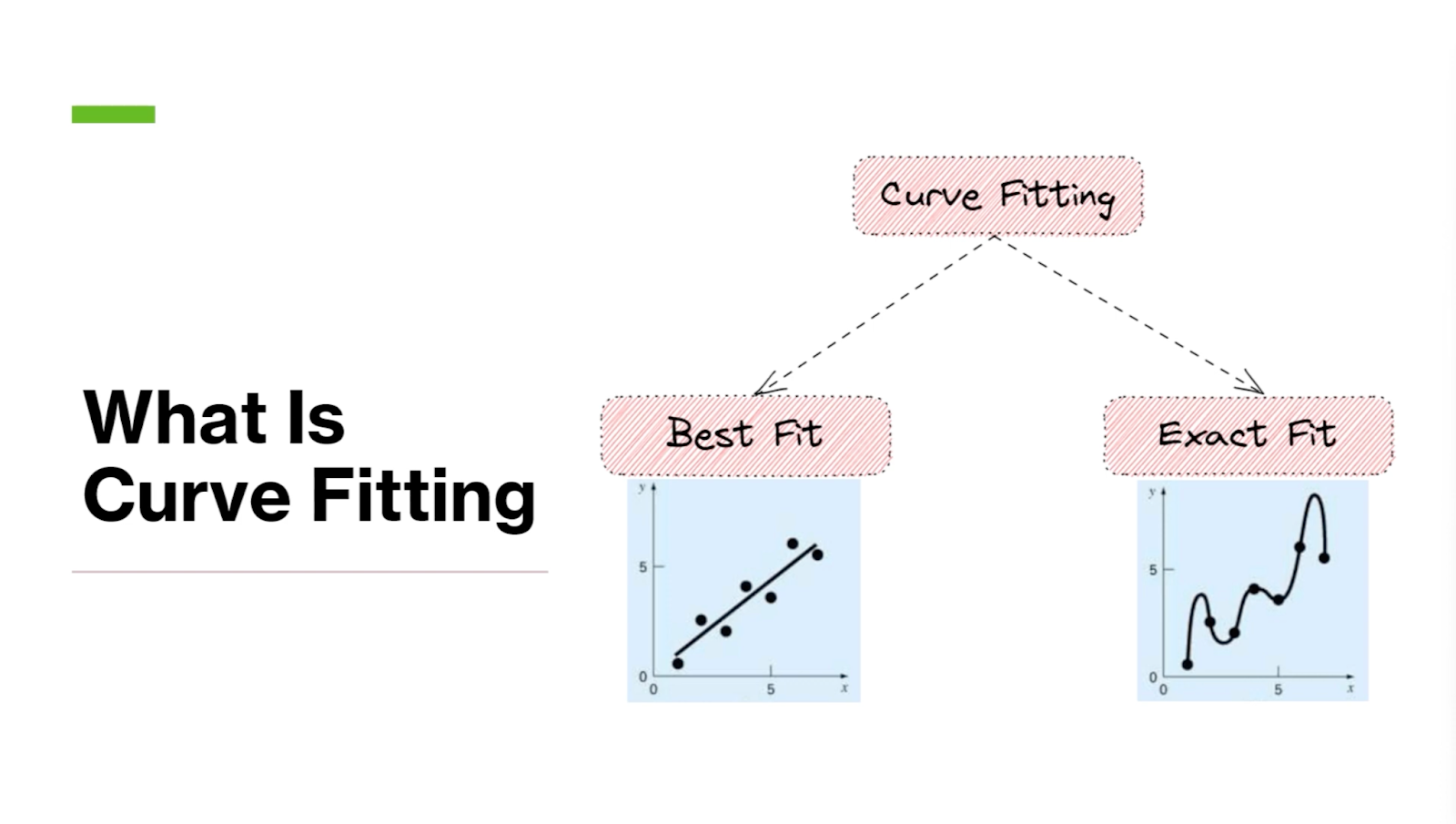

I can’t stress enough the hazards of curve fitting—a pitfall I once slipped into during my early days as a trader.

Curve fitting involves modifying a trading strategy too closely to historical data, a practice that often results in a system incapable of handling different market conditions.

My own misadventure involved developing a strategy based on a limited dataset, only to suffer significant losses when market conditions naturally shifted. The lesson learned is clear: a robust trading strategy demands testing across diverse market cycles to ensure its adaptability.

The Story of Curve Fitting Explained:

To illustrate the concept of curve fitting, Imagine a photographer in a dry forest assuming it won’t rain and building a weak shelter. When heavy rain suddenly comes, the shelter falls apart. Similarly, traders relying only on recent market trends might find themselves unprepared when things unexpectedly change.

Understanding Market Cycles:

A critical question arose in our discussion: How far back should one look to ensure a strategy is well-equipped for different market cycles?

It’s not just about bullish, bearish, or sideways markets; it’s about understanding the significance of volatility within those cycles. A strategy must be strictly tested over several years and spread over various market conditions to truly prove its reliability.

Determining System Viability:

The question persists: Can a trading strategy ever become outdated?

My argument is that if a strategy undergoes thorough testing across different market cycles, the likelihood of failure decreases. The true challenge arises when traders test strategies with limited data or within a short timeframe. I recall spending months developing a strategy, only to realize its lack of practicality due to curve fitting.

The Role of Expectancy and Profit Factor:

In our discussion, we emphasized the importance of calculating expectancy and profit factor to measure a strategy’s feasibility.

Expectancy, determined by the probability of winning and losing trades multiplied by their respective average sizes, provides a comprehensive view of a strategy’s potential.

The formula is as follows:

Expectancy Ratio = (Reward-to-Risk Ratio X Win Ratio) - (Loss Ratio)

A higher profit factor, calculated by multiplying the average profit with the number of profitable trades and doing the same for losses, signifies a more robust system.

Key Strategies for Long-Term Success:

To navigate the challenges of trading, I shared insights gathered from successful fund managers.

Implementing a stop loss for the overall strategy, utilizing an equity curve trendline, and diversifying strategies emerged as primary practices.

Maintaining a diversified portfolio of uncorrelated strategies and adjusting position sizes based on market conditions can help mitigate risk and ensure a smoother equity curve.

QuantMan stands out as a widely used algorithmic trading platform, offering a comprehensive suite of tools for analyzing diverse performance metrics associated with your trading strategy.

These metrics includes important aspects such as risk per trade, maximum drawdown, average profit, average loss, Winning probability, and Winning/Losing Streak for the backtested system, etc. Armed with this data, one can make informed decisions about the potential future performance of the trading strategy.

Here are some of the benefits of using QuantMan Algo Trading:

- It can help traders to save time and effort by automating their trading.

- It can help traders reduce their risk by allowing them to backtest their strategies on historical data.

- It can help traders improve their performance by providing them with all the important trading metrics that we have discussed above.

- It is relatively easy to use, even for traders without coding knowledge.

To learn more about Quantman, please click on this link: https://www.quantman.in/faq/

Conclusion:

In the ever-evolving landscape of trading, strategies may face challenges, but they don’t necessarily become outdated or stop working. The key lies in comprehensive testing, adaptability, and a disciplined approach. By embracing the principles of solid strategy development and remaining vigilant to market changes, traders can enhance their prospects for long-term success.